Policy

Quick summary

- The data burden is the most immediate preparation challenge. Accurate CBAM liability calculation requires embedded carbon data from overseas suppliers. Building supplier engagement and data collection processes now is considerably more efficient than doing so under the 2027 deadline pressure.

- The UK CBAM comes into force on 1 January 2027. It applies a carbon price to imports of aluminium, cement, fertilisers, hydrogen, and iron and steel into the UK. The compliance obligation sits with the UK importer, not the overseas manufacturer.

- The levy is based on the gap between the carbon price paid in the country of origin and the UK carbon price. Suppliers in countries with strong carbon pricing can have that cost deducted, so the mechanism directly rewards supply chains in well-regulated markets.

The UK has built its domestic climate policy around the UK Emissions Trading Scheme (UK ETS), which puts a carbon price on emissions from UK producers. However, a carbon price only works as intended if it can avoid pushing production to countries where no equivalent price applies. This is known as carbon leakage, and the UK Carbon Border Adjustment Mechanism (CBAM) is designed to address it.

The UK CBAM will commence on 1 January 2027. It places a carbon price on imports of certain goods into the UK, ensuring that overseas producers face a comparable carbon cost to their UK counterparts. For UK businesses that import goods in the sectors it covers, the CBAM introduces a new compliance obligation. Importers must report the embedded carbon in qualifying goods and pay a levy based on the difference between the carbon price paid in the country of origin and the equivalent UK ETS cost.

What is the UK CBAM?

The UK CBAM is a mechanism that applies a carbon price to imports of specified goods from countries where carbon pricing is lower than in the UK. Its purpose is to level the playing field: a UK steel producer pays for its carbon emissions under the UK ETS, while an overseas competitor exporting the same steel into the UK may face no equivalent cost. The CBAM closes that gap by applying a charge at the border.

The charge is calculated based on the carbon embedded in the imported goods and the difference between the carbon price already paid in the country of origin and the UK carbon price. This means imported goods face a comparable carbon cost to those made in the UK, so overseas producers cannot undercut UK manufacturers simply by operating in a less regulated market.

The CBAM price is linked directly to the UK ETS. If a supplier in another country has already paid a carbon price equivalent to the UK rate, that can be deducted from the CBAM liability. The mechanism therefore rewards suppliers operating in countries with robust carbon pricing, and creates an incentive for trading partners to strengthen their own carbon pricing frameworks over time.

Which sectors and products are in scope?

The UK CBAM covers five sectors: aluminium, cement, fertiliser, hydrogen, and iron and steel. Ceramics and glass appeared in earlier government consultations but are not in the final scope. Companies that anticipated coverage of those categories should check the commodity code annex in the HMRC policy documents before finalising their compliance assessment.

The liability sits with the UK importer. If your business brings qualifying goods into the UK, the CBAM charge is yours to calculate, report, and pay, regardless of where the goods were produced or what carbon costs the manufacturer faced in their home country. This applies across the whole of the UK, including Northern Ireland, from 1 January 2027.

One area still being worked through is the emissions boundary. Scope 1 direct emissions embedded in imported goods are confirmed in scope. The inclusion of indirect emissions, covering Scope 2 and Scope 3, has been delayed until 2029 at the earliest. Only Scope 1 direct emissions are in scope from the January 2027 start date.

How will the UK CBAM work in practice?

Importers of qualifying goods will need to register with HMRC, report the embedded carbon in their imports, and pay the CBAM levy on a regular reporting cycle. The levy is calculated as the difference between the carbon price already paid in the country of origin and the equivalent UK carbon price. Importers whose total value of CBAM goods falls below £50,000 in a given period are not required to register.

Some key elements, including the calculation methodology and verification requirements, are still being finalised through secondary legislation. Draft regulations were published in February 2026, with a second set expected in Spring 2026. Companies should monitor HMRC guidance as it is published, since the rules may still shift before January 2027.

The most immediate practical challenge is data. To calculate the levy accurately, importers need verified emissions figures from their overseas suppliers, specifically the actual carbon embedded in the goods rather than HMRC default values. Default values will be available, but they are likely to be set conservatively. Importers relying on them may end up paying more than those who obtain actual figures from suppliers. Starting supplier engagement now, well ahead of the 2027 deadline, is the most effective way to close that gap.

How does the UK CBAM compare to the EU CBAM?

Many UK businesses will already be tracking the EU Carbon Border Adjustment Mechanism (EU CBAM), which entered its transitional reporting phase in October 2023 and moves to full operation in 2026. The two mechanisms share the same underlying logic but apply in different directions. The EU CBAM applies to goods exported into the EU. The UK CBAM applies to goods imported into the UK. A company exporting steel from India into both the EU and the UK may face obligations under both mechanisms, with different calculation methodologies, reporting formats, and deadlines to manage.

The sectoral scope is also slightly different. The EU CBAM covers aluminium, cement, electricity, fertilisers, hydrogen, and iron and steel. The UK CBAM covers aluminium, cement, fertilisers, hydrogen, and iron and steel, with electricity excluded at launch. Companies trading into both the EU and UK should assess their exposure under both mechanisms separately rather than assuming alignment.

What should affected businesses do now?

The 2027 start date may feel distant, but the preparation work is not. Three actions are worth prioritising now:

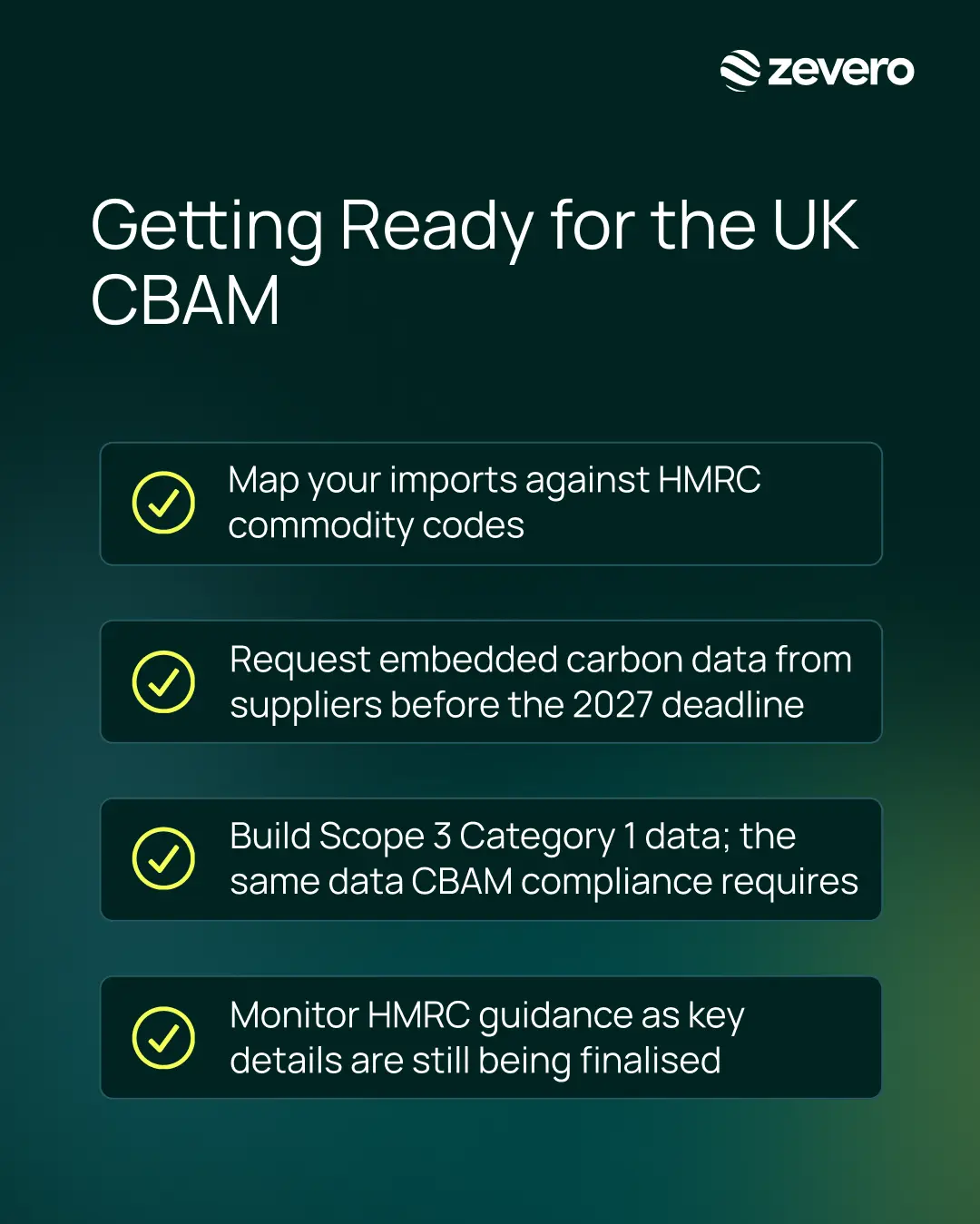

Map your imports against the in-scope sectors. Identify which of your imported goods fall within the five sectors in scope and which suppliers are affected. Use HMRC's commodity code annex to verify whether specific products are included or excluded.

Start supplier engagement early. The CBAM liability calculation requires embedded carbon data from your overseas suppliers. Gathering, verifying, and formatting that data takes time, particularly for suppliers in countries without established carbon reporting practices. The earlier you start those conversations, the better.

Build your Scope 3 data capability. If your business does not already track Scope 3 Category 1 emissions from purchased goods and services, the UK CBAM creates a direct financial incentive to start. The embedded carbon data required for CBAM compliance is the same data that feeds Scope 3 Category 1 calculations. Companies that build this capability now serve two purposes at once.

Monitor HMRC guidance. Secondary legislation is still being finalised. The calculation methodology, verification requirements, and reporting format will be confirmed in further guidance from HMRC. Stay close to the CBAM policy pages on GOV.UK and consider joining the HMRC CBAM mailing list.

How Zevero can help

The UK CBAM turns supply chain carbon data into a direct financial obligation. The embedded emissions in your imported goods will determine what you owe. Companies that already have structured, verified Scope 3 data from their suppliers will be in a significantly better position than those starting from scratch in 2026.

Zevero helps UK importers build that foundation:

- Support supplier outreach and data collection, so verified embedded carbon figures are available when you need them rather than when the deadline forces the issue

- Connect CBAM compliance data to your broader Scope 3 inventory, so the embedded emissions work you do for CBAM directly feeds your Category 1 calculations without duplication

Secondary legislation is still being finalised, supplier data takes time to gather, and HMRC registration will need to be in place before the first imports are made. Speak to the Zevero team about getting your supply chain emissions data ready.

FAQs

What happens if my supplier cannot provide embedded carbon data?

When do businesses need to register for the UK CBAM?

Does the UK CBAM apply to goods that pass through the UK on their way to another destination?

Will the UK CBAM expand to cover more sectors in future?

How does the UK CBAM interact with existing trade agreements?

Related posts

Read more

Blog

Mar 30, 2026

CBAM Compliance: Collecting Supplier Emissions Data

CBAM Compliance: Collecting Supplier Emissions Data

Read more

Blog

Feb 5, 2026

CBAM Explained: The EU Carbon Border Adjustment Mechanism

CBAM Explained: The EU Carbon Border Adjustment Mechanism

See how Zevero can streamline your carbon reporting

Grow your business and reduce your impact