Policy

In February 2026, the Korea Sustainability Standards Board (KSSB) published the first set of Korean Sustainability Disclosure Standards (KSDS): KSDS 1 and KSDS 2. The day before, the Financial Services Commission (FSC) published a draft roadmap setting out who must report, and when. South Korea joins Japan, Australia, Singapore, and the Philippines as part of a broader APAC shift toward mandatory, internationally aligned disclosure. For multinationals with exposure to Korean markets or supply chains, this is worth tracking now, not when the mandate lands.

What are the KSDS?

The KSDS are South Korea's national sustainability disclosure standards, built on the International Sustainability Standards Board's (ISSB) IFRS S1 and IFRS S2. KSDS 1 covers general requirements for sustainability-related financial disclosures. KSDS 2 covers climate-related disclosures specifically. Both require companies to report across four core areas: governance, strategy, risk management, and metrics and targets. The standards are designed to be interoperable with the ISSB baseline, meaning disclosures produced under KSDS should be recognisable and comparable to those produced under IFRS S1 and S2 in other markets.

Who needs to report, and when?

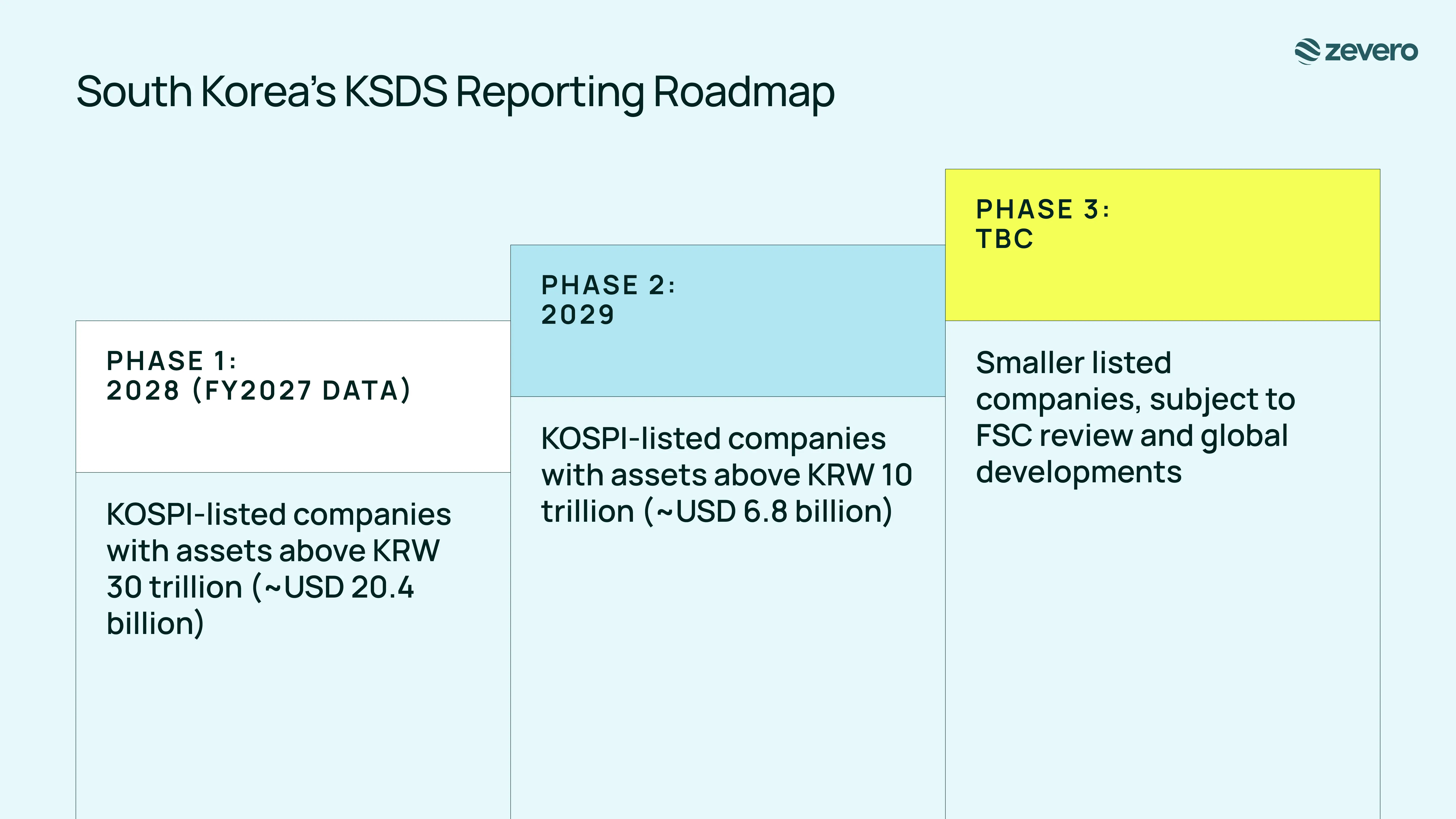

The FSC's draft roadmap proposes a phased rollout tied to company size:

- 2028 (reporting on FY2027 data): large companies listed on KOSPI (Korea Composite Stock Price Index, South Korea's main stock exchange benchmark) with assets above KRW 30 trillion (approximately USD 20.4 billion).

- 2029: potential expansion to companies with assets above KRW 10 trillion (approximately USD 6.8 billion).

- Further expansion beyond KRW 10 trillion is under consideration, with timing dependent on how other major markets progress and how prepared Korean companies are at that stage.

The roadmap was open for public consultation and the FSC planned to confirm the final version in April 2026. Companies should check for the finalised roadmap before making compliance assumptions.

How do the KSDS differ from the ISSB baseline?

The KSSB based the standards on the ISSB's IFRS S1 and IFRS S2, while tailoring certain requirements to the domestic context. The key differences are:

- Scope 3 deferral: A three-year deferral on Scope 3 value chain emissions disclosure. The ISSB's own transitional relief was one year. This gives Korean companies more time to build supply chain data capability, but it does not remove the obligation permanently.

- Climate-first focus: Non-climate sustainability disclosures under KSDS 1 remain optional for now. Companies can focus on climate reporting before broadening to wider sustainability topics.

- Assurance: Third-party assurance starts as optional, with mandatory adoption to be phased in over time.

- Publication timing: Companies are not required to publish sustainability disclosures simultaneously with their financial statements, unlike the ISSB baseline.

These are pragmatic design choices that reduce the initial implementation burden while keeping the direction of travel clear. The KSSB has stated its intention to gradually increase alignment with ISSB standards over time.

Why this matters beyond Korea

For multinationals, the practical implication is not just about direct compliance. Korean companies in Tier 1 will begin reporting on FY2027 data, meaning their own suppliers and partners may face indirect disclosure pressure before the mandate formally extends to them. If your company supplies into Korean markets or has Korean counterparts in your value chain, their reporting requirements will start generating data requests upstream.

Korea's move is also part of a wider pattern. APAC is not adopting a single uniform framework: Japan, Australia, Singapore, and the Philippines have each developed national standards that align with, but are distinct from, the ISSB baseline. For multinationals operating across the region, a consistent internal data infrastructure is the most practical response to this patchwork of interoperable-but-distinct requirements.

How to prepare for KSDS reporting

The mandate is not live yet, but the standards are published and the roadmap is being finalised. Three practical steps worth taking now:

- Run a gap analysis against IFRS S1 and S2, which underpins the KSDS. Closing gaps against the global baseline covers most of what Korea will require.

- Establish your Scope 1 and 2 baseline before turning to Scope 3. The three-year Scope 3 deferral provides breathing room, but the underlying data work takes time.

- Check whether your Korean partners or customers fall into the first reporting tier. Indirect pressure from their disclosure requirements may arrive before your own mandate does.

Whether you are preparing for a first filing or getting ahead of indirect pressure from Korean partners and customers, measuring your company's carbon footprint is the right place to start.

Thanks for reading!

An Introduction to Korea's Sustainability Reporting (KSDS)

Add us as a preferred source

Related posts

Read more

Blog

Apr 13, 2026

Philippines Sustainability Reporting: A Guide to PFRS S1 and S2

Philippines Sustainability Reporting: A Guide to PFRS S1 and S2

Read more

Blog

Mar 10, 2025

Japan's SSBJ Standards: What Companies Need to Know

Japan's SSBJ Standards: What Companies Need to Know

Read more

Blog

Oct 3, 2024

Preparing for SGX’s New Climate Reporting Mandates: What You Need to Know

Preparing for SGX’s New Climate Reporting Mandates: What You Need to Know

See how Zevero can streamline your carbon reporting

Grow your business and reduce your impact