Policy

.webp)

On 3 July 2026, the European Commission adopted two delegated acts that settle a question the market has been asking since the Omnibus I simplification process began: what will companies actually have to report under the revised European Sustainability Reporting Standards (ESRS), and who gets protected from trickle-down data requests.

One act revises the ESRS themselves. The other establishes, for the first time, a standalone voluntary reporting standard for smaller companies, which also sets a hard "value chain cap" on what larger companies can demand from suppliers. Both are now with the European Parliament and Council for scrutiny. Below is what's confirmed, what changed since EFRAG's technical advice, what didn't change despite pressure to drop it, and what to do next.

From technical advice to adopted law

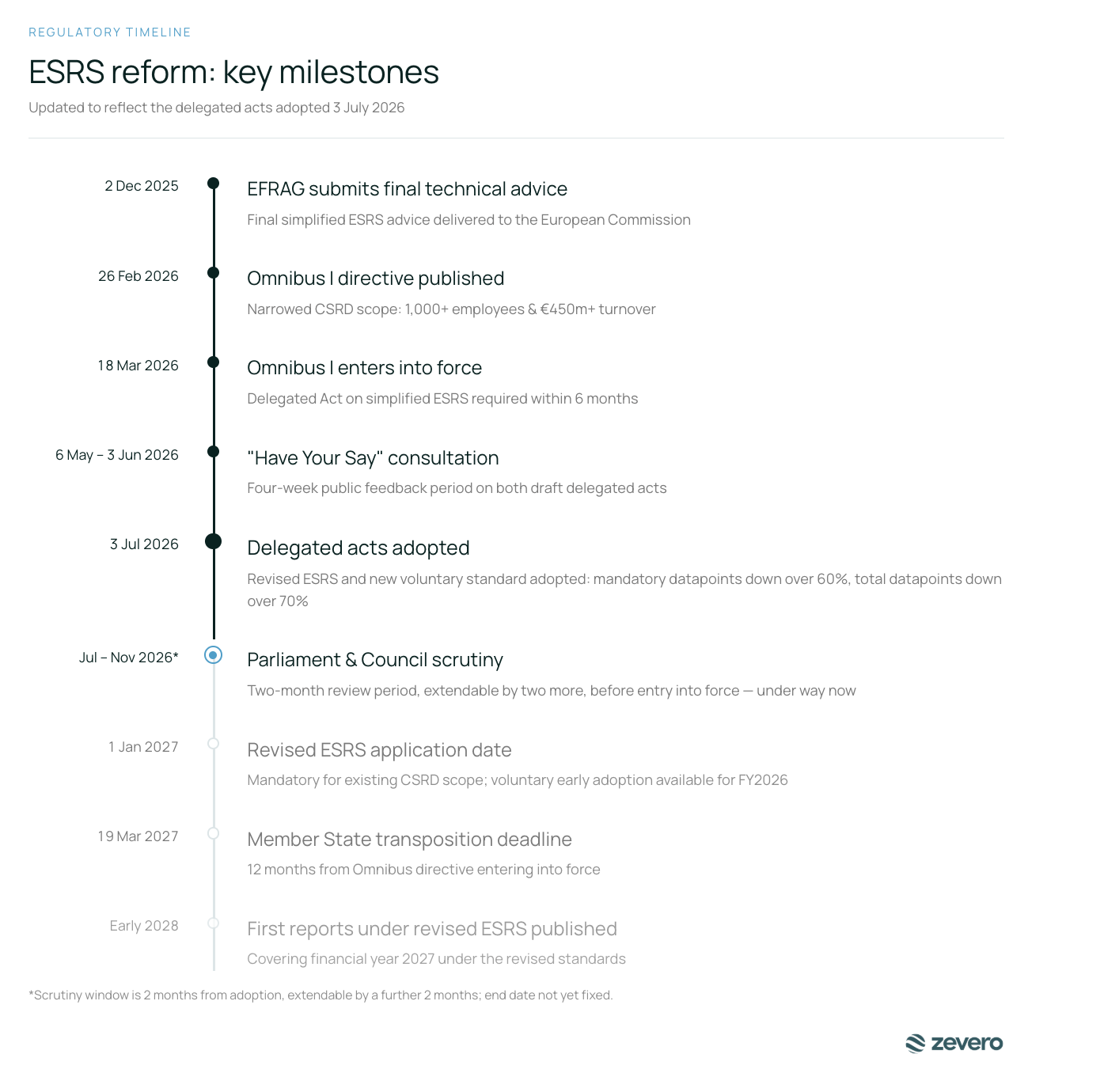

EFRAG submitted its final technical advice on the revised ESRS to the Commission on 2 December 2025, following a public consultation that ran from 29 July-29 September 2025. That advice proposed cutting mandatory datapoints by 61% and removing voluntary ("may disclose") datapoints entirely. The Commission then ran its own consultation process, jointly with the Member State Expert Group on Sustainable Finance and the Accounting Regulatory Committee, alongside several other groups. Both delegated acts were also opened for a four-week public consultation from 6 May-3 June 2026, which drew 453 responses on the revised ESRS and 203 on the voluntary standard.

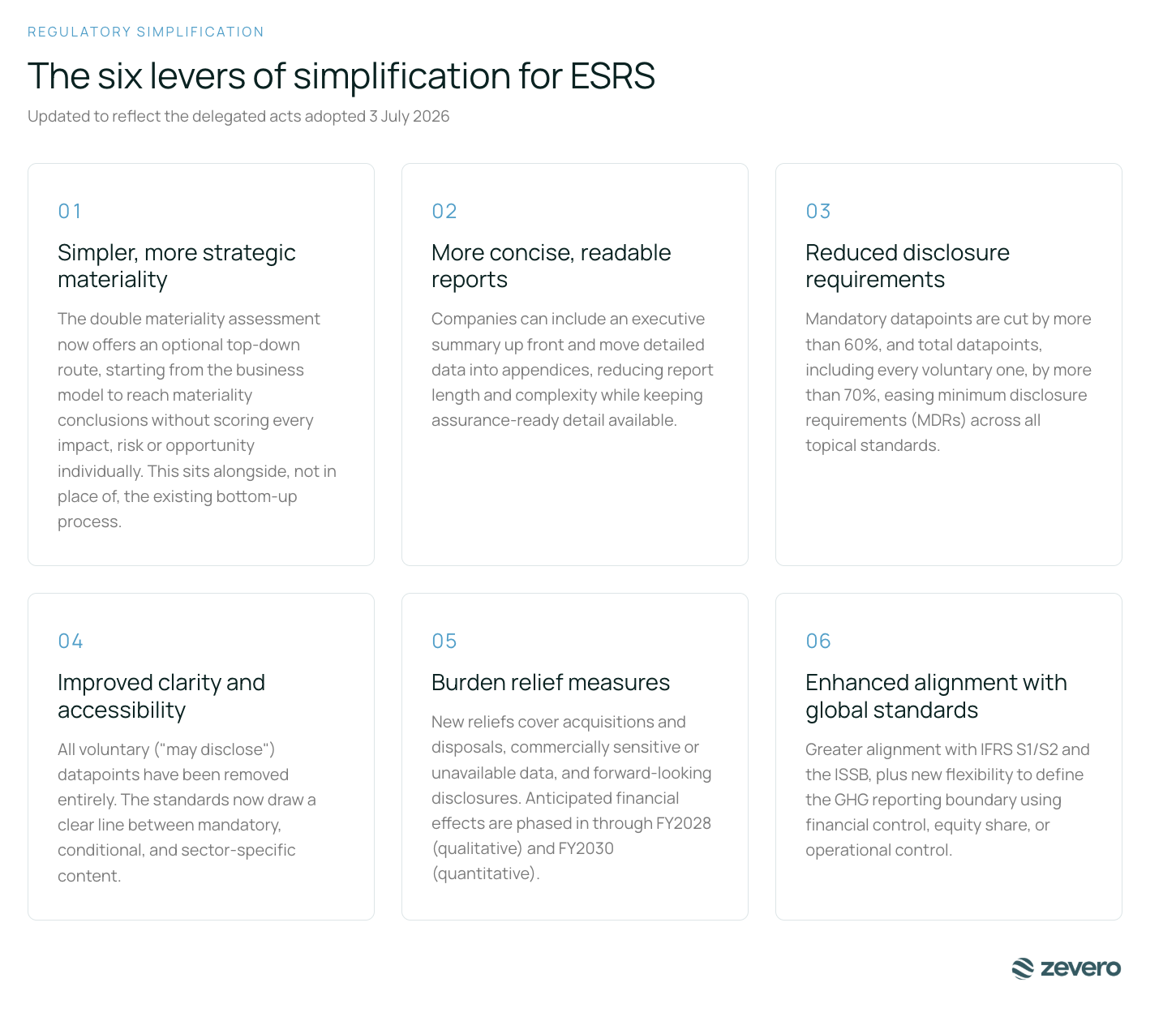

The result, adopted 3 July 2026: mandatory datapoints down by more than 60%, and total datapoints (including the voluntary ones EFRAG proposed removing) down by more than 70%. The Commission expects this to cut reporting costs by more than 30% per company on average, ahead of its own 25% burden-reduction target. Full background on the CSRD and how it fits together sits on the Commission's corporate sustainability reporting hub.

What survived, and what didn't

Simplification invites an assumption that everything got lighter. It didn't. Some of the most-lobbied-for changes never made it into the adopted text.

Double materiality stayed intact

Despite sustained pressure, including from German corporates and the ISSB itself, to move ESRS toward a single financial-materiality lens, the Commission kept double materiality as the basis for reporting. Companies still assess both their impact on people and the environment, and the financial risks and opportunities sustainability issues create for them. What changed is the process for getting there, not the underlying obligation.

Nothing was deleted at the standard level

All twelve topical standards remain, as do the two cross-cutting standards ESRS 1 and ESRS 2, which carry the concepts, principles, and general disclosure requirements that everything else plugs into. What shrank is the datapoint list inside each one.

What actually changed:

- An optional top-down route into materiality, sitting alongside the existing bottom-up process (more below).

- Non-material information now falls under "shall not report" rather than the softer "is not required to report."

- Fair presentation is assessed at the level of the whole statement, not per datapoint.

- The GHG reporting boundary can now be set via financial control, equity share, or operational control.

- Climate transition plans must flag explicitly if targets aren't compatible with 1.5°C.

- Anticipated financial effects follow a longer phase-in than EFRAG proposed: qualitative from FY2028, quantitative from FY2030.

- Microplastics reporting narrowed to primary microplastics only.

- Materiality of pollutants is now a managerial assessment tied to the company's activities and sector, not a fixed list.

- Substances of very high concern get a one-year phase-in, running through FY2028, for undertakings that are users of articles containing them.

- Human rights and discrimination incidents are limited to "substantiated verified" instances.

- Financial institutions managing fiduciary-mandate investments can exclude those investments from their sustainability statement, since SFDR and related rules already cover the relevant sustainability matters.

- Companies can omit information that would be seriously prejudicial to their commercial position, trade secrets, classified information, or information otherwise protected by law, provided they disclose that the exemption was used and reassess it each reporting period.

A materiality detail worth knowing

The adopted text keeps a "gross versus net" clarification that's easy to miss. When assessing the severity of an actual negative impact, a company accounts for how it was already mitigated in previous periods, but can't factor in remediation carried out during the current reporting period itself. For potential negative impacts, mitigation actions can only be factored into severity or likelihood if those actions are already implemented and can reasonably be assumed to work; policies that exist on paper but haven't been rolled out don't count. It's a small provision with a real effect on how generously a company can score its own progress.

Standard by standard: What's actually different

The headline datapoint cuts land unevenly across the twelve standards. Here's what changed in each, confirmed directly against the adopted annexes.

E1 Climate Change came through the most intact. It keeps its full Scope 1, 2 and 3 structure, its transition plan requirement, and is the only environmental standard that retains a complete anticipated financial effects disclosure. The GHG boundary flexibility (financial control, equity share, or operational control) applies here.

E2 Pollution narrows to primary microplastics only, and which pollutants count as material is now a managerial call based on the company's sector and activities rather than a fixed list.

E3 Water and Marine Resources keeps total water withdrawal and total water discharge as core disclosures.

E4 Biodiversity and Ecosystems retains its own transition plan disclosure requirement: if a company has a biodiversity and ecosystems transition plan aligned with the Global Biodiversity Framework, it discloses that. E4 is also one of the standards Wave 1 companies can phase in later (more below).

E5 Resource Use and Circular Economy explicitly picks up critical and strategic raw materials, as defined under the EU Critical Raw Materials Act, as something companies disclose where relevant to resource inflows.

S1 through S4 (Own Workforce, Workers in the Value Chain, Affected Communities, and Consumers and End-users) are explicitly aligned in content and structure. S2 covers the same sub-topics as S1 for workers in the value chain who aren't part of the company's own workforce, which is designed to stop the same ground being covered twice under different headings.

G1 Business Conduct keeps its scope: anti-corruption and anti-bribery culture, whistleblower protection, animal welfare, supplier payment practices (including late payment to SMEs), and political influence and lobbying activity.

Both S2, S3, and S4, along with E4, are on the list of standards that larger Wave 1 companies (those already over the €450 million turnover and 1,000 employee thresholds) can omit entirely for financial years before 2027, and other undertakings can omit for their first two years of reporting.

The value chain cap is now a real, standalone standard, not a scope note

The earlier draft guidance simply said value chain requests to smaller suppliers "should not exceed VSME scope." That's no longer just guidance. The Commission has adopted a dedicated voluntary reporting standard, based on, and replacing, the VSME Recommendation, that does two things at once:

- It gives companies with 1,000 or fewer employees a standardised, proportionate framework to report sustainability information voluntarily, structured as a Basic Module (the target for micro-undertakings, and the floor for everyone else) and a Comprehensive Module.

- It sets the value chain cap itself: companies subject to mandatory CSRD reporting cannot require more from a protected supplier than what's listed in a dedicated annex to the new standard. That annex sets two separate lists: one for suppliers with 10 employees or fewer, and a broader one for suppliers with more than 10 (but no more than 1,000) employees.

The detail worth flagging to any supplier relying on this cap: Scope 3 GHG emissions data is not on the capped list. The cap also only restricts requests made for the purposes of the requesting company's own CSRD reporting. The same information requested as an ordinary supply contract term, a tender condition, or under other Union or national law sits entirely outside the cap. Suppliers should expect these requests to continue; the cap changes the legal basis on which they can be made, not necessarily the volume.

The VSME Recommendation itself stops producing legal effects once this new delegated act enters into force.

The wider Omnibus I picture these two acts sit inside

The 3 July acts are the ESRS-level follow-through on a broader reform that was already locked in when Omnibus I entered into force on 18 March 2026. Three parts of that broader picture matter for anyone trying to understand the full compliance footprint, and none of them were touched by the July acts because they didn't need to be:

Assurance stayed at "limited"

Omnibus I dropped the original plan to move sustainability statements toward reasonable assurance, the higher bar applied to financial statements. Limited assurance remains the only mandatory requirement, and the Commission still has to adopt harmonised limited assurance standards, now due by 1 July 2027.

Mandatory sector-specific standards were removed entirely

The Commission's power to adopt binding sector-specific ESRS was deleted under Omnibus I. What replaces it is optional Commission guidance illustrating how the general standards apply to a given sector, developed in consultation with stakeholders rather than adopted as binding law.

Financial holding undertakings got a scope carve-out

Parent companies that qualify as financial holding undertakings, meaning their sole purpose is acquiring and managing holdings without directly or indirectly managing the underlying businesses, can choose whether to report or omit consolidated sustainability information at group level.

What's still on the table

A few pieces of the wider framework remain unresolved, and are worth tracking separately from the two acts adopted on 3 July:

- The non-EU standards (NESRS) for third-country groups that fall into CSRD scope but choose not to use the EU ESRS for a globally consolidated statement are still being developed. That work had been paused pending finalisation of the main ESRS revision; EFRAG's 2026 work plan targets delivering technical advice to the Commission by the end of January 2027.

- Detailed implementation guidance, including updated materiality and value chain guidance from EFRAG reflecting the final adopted text, is expected to follow now that the delegated acts are adopted, rather than arriving alongside them.

- The XBRL digital reporting taxonomy tied to the revised standards will be finalised closer to the point the standards actually take effect, rather than at adoption.

None of these change what's mandatory or when for the standards covered in this piece, but they're the natural next things to watch.

Timeline

- 2 December 2025 – EFRAG submitted final technical advice on the revised ESRS to the Commission.

- 18 March 2026 – Omnibus I Directive entered into force, narrowing CSRD scope to companies over 1,000 employees and €450 million turnover.

- 3 June 2026 – Public consultation on both delegated acts closed.

- 3 July 2026 – Both delegated acts adopted by the Commission.

- Now – Both acts sit with the European Parliament and Council for a two-month scrutiny period, extendable by a further two months.

- 19 March 2027 – Deadline for Member States to transpose the Omnibus I Directive's CSRD-related provisions into national law.

- 1 July 2027 – Deadline for the Commission to adopt harmonised limited assurance standards.

- FY2026 – Companies already applying the existing ESRS may voluntarily early-adopt the revised standards, or apply the existing standards with certain new reliefs, provided they state clearly in their sustainability statement which version they're using.

- FY2027 – Revised ESRS become mandatory for companies already in CSRD scope. The value chain cap also goes into effect.

- FY2028 – Qualitative anticipated financial effects and substances of very high concern reliefs expire for the first wave of reporters.

- FY2030 – Quantitative anticipated financial effects and substances of concern reliefs expire.

What should companies do now?

The right next step depends on where a company actually sits, so the guidance splits three ways.

If already reporting under current ESRS (Wave 1, over the new thresholds):

- Decide on early adoption for FY2026, not just eligibility. EFRAG's cost-benefit modelling shows savings starting around 28% of baseline cost in 2027, rising to 38% in 2028, before settling near 33-36%. Waiting for the mandatory 2027 date means starting at the shallow end of that curve by default. Put this in front of your CFO now.

- Review your materiality process. The "shall not report" wording and whole-statement fair presentation standard both raise the bar on documentation, especially if you adopt the top-down shortcut.

- Check which of E4, S2, S3 and S4 you're using the pre-2027 phase-in relief for, and build a real plan for when that relief runs out.

- Confirm your GHG boundary methodology. If you already use equity share or operational control for other reporting, you no longer need to reconcile it to financial control for ESRS.

If newly out of scope, or newly in scope from FY2027 (Wave 2 under the narrowed thresholds):

- Confirm your position under the new €450 million / 1,000 employee thresholds rather than assuming your prior CSRD status still applies.

- If you're now out of scope, don't treat that as the end of the conversation. Your larger customers, lenders, and investors still need the data, and they'll ask for it through contracts and questionnaires rather than CSRD itself.

- If you're newly in scope from FY2027, you go straight to the simplified standards with no transitional period under the original 2023 text. Start building your materiality assessment and data infrastructure now rather than waiting for the scrutiny period to close.

For suppliers relying on the value chain cap:

- Don't assume the cap stops all requests for Scope 3 data.

- Separate requests made for a customer's CSRD reporting (where the cap applies) from requests made under a contract, tender, or other obligation (where it doesn't).

- Prepare a clean, standardised answer to these requests, using the Basic Module of the new voluntary standard as a starting point.

For everyone else:

Track the scrutiny period. Both acts are with the European Parliament and Council now, for two months, extendable by two more. Nothing here is final law until that period closes, so treat the mandatory-from-2027 date as the planning anchor while watching for amendments.

The bigger picture

This simplification lowers the regulatory floor for sustainability disclosure. It does not lower the bar the market applies to carbon claims specifically. Climate came through this revision more intact than any other topic, keeping the only complete anticipated financial effects requirement left among the environmental standards. At the same time, standards bodies outside the EU, including the SBTi’s Corporate Net-Zero Standard V2.0 and the ISO 14060 draft standard, are tightening what counts as a credible claim in the same window that ESRS loosened what counts as compliant.

Companies that read this update as a reason to invest less in carbon measurement are reading it backwards. The compliance requirement got lighter, but the credibility requirement did not.

Zevero will continue to track this as both delegated acts move through Parliament and Council scrutiny. Get in touch with our team if you want help mapping your reporting approach against the adopted text.

Related posts

Read more

Blog

Feb 26, 2025

The EU Omnibus Proposal: What It Means for Your Sustainability Reporting

The EU Omnibus Proposal: What It Means for Your Sustainability Reporting

Read more

Blog

Feb 12, 2025

What is CSRD? How the Corporate Sustainability Reporting Directive Impacts Businesses Worldwide

What is CSRD? How the Corporate Sustainability Reporting Directive Impacts Businesses Worldwide

.webp)

Read more

Blog

Jul 30, 2025

Navigating the VSME: EU Sustainability Reporting Standards for SMEs

Navigating the VSME: EU Sustainability Reporting Standards for SMEs

See how Zevero can streamline your carbon reporting

Grow your business and reduce your impact