Policy

Quick summary

- The burden of proof stays with the business. Under Bill C-59, companies must substantiate environmental claims before being challenged, not after.

- Substantiation standard loosened for business-level claims. The requirement was relaxed in March 2026, though product-level claims still require adequate and proper testing.

- Private lawsuits narrowed, but Bureau enforcement continues. Business-level claims are no longer open to private legal action, though product-level claims still are, and the Competition Bureau retains full enforcement power.

- Recognised methodology remains the strongest defence. The GHG Protocol isn't a legal requirement for business claims anymore, but it's still the best way to demonstrate substantiation; vague claims like "sustainable" stay highest-risk.

Canada's Bill C-59, the Fall Economic Statement Implementation Act, 2023, took effect on June 20, 2024, amending the Competition Act to introduce new anti-greenwashing provisions. The changes affect any business making public environmental claims in Canada, whether in advertising, on product labels, on a website, or in a sustainability report used for marketing purposes.

The law is not designed to stop companies from talking about their environmental performance. It is designed to ensure that what they say can be backed up. The Act requires that certain environmental claims about a business or its activity be adequately and properly substantiated before they are made. This blog is not a legal guide. It is a practical explanation of what that substantiation requirement means, which types of claims carry the most risk, and what defensible environmental claims look like in practice.

What changed under Bill C-59

The amendments introduce two new substantiation requirements for environmental claims, both of which came into force on June 20, 2024.

- Section 74.01(1)(b.1) covers product-level claims. Parties making public statements about a product's environmental benefits must support those statements with an adequate and proper test.

- Section 74.01(1)(b.2) covers business-level claims. Parties making representations about the environmental benefits of a business or business activity must base those statements on adequate and proper substantiation. As of March 26, 2026, this no longer has to follow an internationally recognised methodology, that specific requirement was removed by Bill C-15, the Budget 2025 Implementation Act. Product-level claims under s.74.01(1)(b.1) are unaffected and still require adequate and proper testing.

Critically, both provisions reverse the burden of proof. Under the old regime, the regulator had to prove a claim was false. Under Bill C-59, the company making the claim must be able to prove it stands up to scrutiny.

From June 2025 to March 2026, private parties including environmental groups, competitors, and consumers could bring greenwashing claims about business-level statements directly before the Competition Tribunal. A subsequent amendment removed that route for business-level claims specifically. Private parties can still bring direct Tribunal action for product-level claims, and the Competition Bureau retains its own enforcement powers across both provisions.

Penalties for non-compliance

The Competition Bureau has made clear that the penalties for non-compliance are significant. An administrative monetary penalty can be assessed against a corporation for the greater of $10 million for the first order and $15 million for any subsequent order, and 3% of the corporation's annual worldwide gross revenues. The penalty applied is whichever of these figures is higher.

Beyond financial penalties, the Competition Tribunal can order a company to cease making the claim, publish a corrective notice, and repay affected parties. Even where no penalty is ultimately imposed, a Bureau investigation or private Tribunal application carries significant reputational and legal costs that are difficult to quantify in advance.

What counts as "adequate and proper substantiation" now

Following the March 2026 amendments, business-level environmental claims no longer need to point to a specific internationally recognised methodology. In practice, this doesn't mean the substantiation bar has disappeared,it means businesses have more flexibility in how they meet it. The Competition Bureau's finalised guidelines, issued June 5, 2025, are being updated to reflect the amendment, but the underlying principle is unchanged: claims must be based on evidence that is fit, suitable, and proportionate to what's being claimed.

These frameworks are no longer a legal requirement for business-level claims, but they remain the strongest evidence a business can offer. For emissions-related claims, the GHG Protocol is still the most defensible basis. For offset-based claims, Verra's Verified Carbon Standard (VCS) and the Gold Standard remain the leading substantiation frameworks. Using a recognised methodology, even where it's no longer mandated by statute, is the clearest way to demonstrate "adequate and proper" substantiation if a claim is ever challenged.

The Bureau's position is that businesses should choose substantiation that is suitable, appropriate, and relevant to the claim, and thorough enough to establish it. Third-party verification will be required where it is called for by the methodology being relied upon.

The more ambitious the claim, the more rigorous the substantiation required to support it. A specific percentage reduction claim against a defined baseline requires less documentation than a carbon neutrality claim, which demands full scope coverage, verified offsets, and a documented residual emissions position.

Common claim types and their risk profiles

Carbon neutral

Carbon neutral is one of the highest-risk claims a company can make. A defensible carbon neutrality claim requires full Scope 1, 2, and 3 emissions measurement, clear documentation of what residual emissions remain, and verified, high-quality offsets to cover them. Companies that claim carbon neutrality based on Scope 1 and 2 data only, without disclosing that Scope 3 is excluded, are most exposed.

Net zero target claims

Announcing a net zero target is not the same as substantiating one. The claim needs a documented reduction pathway behind it, not just a date. Validation through the Science Based Targets initiative (SBTi) is one recognised route. Without that pathway, a net zero commitment is a future claim with nothing currently behind it, and the burden of proof sits with the company making it.

X% reduction in emissions

Relative claims are lower risk than absolute ones, but only when the basis is transparent. A 30% reduction claim is defensible if the baseline year, the emissions boundary, the methodology, and the data sources are clearly stated and auditable. The most common vulnerability is presenting a Scope 1-only reduction as a company-wide figure without disclosing that Scope 2 and 3 are excluded.

Sustainable / eco-friendly / green

Vague terms with no measurable basis behind them carry the highest risk. Without a specific standard or criterion to point to, these claims are very difficult to substantiate under any recognised methodology and are the most likely to attract attention from the Competition Bureau or private litigants.

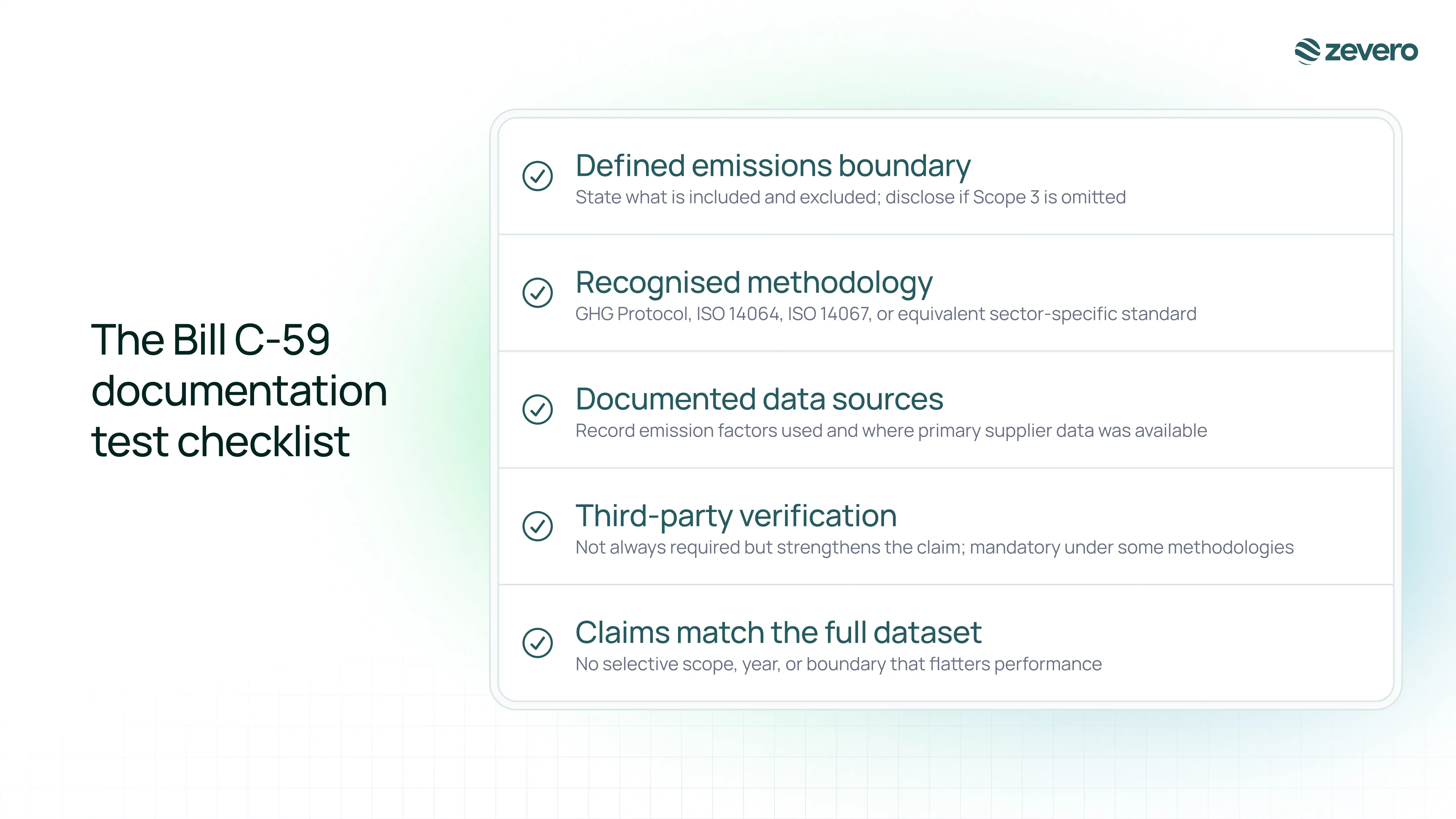

What defensible looks like: the documentation test

A useful way to assess whether a claim is defensible is to consider what documentation exists to support it if the Competition Bureau were to investigate tomorrow. A defensible claim typically has the following elements in place:

- A defined emissions boundary. State clearly what is included and what is excluded. If Scope 3 is omitted, say so. If the claim covers only part of the product lifecycle, declare the boundary.

- A recognised methodology. Since March 2026, using an internationally recognised methodology is no longer a strict legal requirement for business-level claims, but the GHG Protocol, ISO 14064, ISO 14067, or a recognised sector-specific standard remains the most defensible basis for any calculation, and the strongest evidence to offer under the current "adequate and proper substantiation" standard.

- Documented data sources. Record where the underlying emissions data came from, including which emission factors were used and where primary supplier data was or was not available.

- Third-party verification where possible. Not always required, but it strengthens the claim significantly and is mandatory under some methodologies. Where verification has been obtained, state who carried it out and under which standard.

- Claims that reflect what the data actually shows. Selecting a favourable baseline year or a narrow boundary to make performance appear stronger than it is creates direct exposure under Bill C-59.

Building and maintaining documentation is not just a substantiation requirement. It is the foundation of the due diligence defence available under the Act. That defence protects businesses that can show they took genuine, documented steps to ensure claims were properly supported before making them.

What this means for sustainability programmes

Bill C-59 does not prevent companies from talking about their environmental performance. It requires that what they say can be backed up. Companies can only claim what they can show, and every public environmental claim is now a potential liability without the data and methodology to support it.

The businesses most exposed are not those that communicate too much, but those that communicate things they cannot substantiate. Better data supports better claims, stronger disclosures across frameworks including CSRD and CSDS, and more informed business decisions. Measurement rigour is not a compliance cost. It is what makes a sustainability programme credible.

How Zevero can help

Defensible claims under Bill C-59 depend on three things: a recognised methodology, traceable data, and documentation that can be produced on demand.

Zevero's carbon management platform produces GHG Protocol-aligned emissions calculations across Scope 1, 2, and 3, with full methodology documentation and traceable data sources built into every calculation. For companies that need to structure existing data into framework-aligned disclosures, our AI-powered ESG Reporting Tool converts your documents into audit-ready reports.

FAQs

Does Bill C-59 apply to sustainability reports as well as advertising?

Does Bill C-59 apply to companies headquartered outside Canada?

What is the due diligence defence under Bill C-59?

Can a company be penalised for a claim it made before Bill C-59 came into force?

How does Bill C-59 interact with voluntary sustainability frameworks like CDP or GRI?

Thanks for reading!

How to Make Defensible Environmental Claims Under Canada's Bill C-59

Add us as a preferred source

Related posts

%20(1).webp)

Read more

Blog

May 26, 2026

Understanding Canada's Sustainability Disclosure Standards

Understanding Canada's Sustainability Disclosure Standards

Read more

Blog

Jul 31, 2025

ISO 14064 vs ISO 14067: The Standards Behind Organisational and Product Carbon Reporting

ISO 14064 vs ISO 14067: The Standards Behind Organisational and Product Carbon Reporting

Read more

Blog

Mar 26, 2025

Understanding SBTi and Setting Climate Targets for Your Business

Understanding SBTi and Setting Climate Targets for Your Business

See how Zevero can streamline your carbon reporting

Grow your business and reduce your impact